If you’re a Washington homeowner trying to figure out what is roofing repair credit and whether it can help you pay for a damaged or aging roof, you’re not alone in the confusion. Many homeowners search for federal tax credits in 2026, only to discover the landscape shifted at the end of 2025. The good news: real options still exist. From tax credits on 2025 installations to SBA disaster loans triggered by recent flooding across Washington, this guide lays out every practical financing path available to you right now, with no guesswork required.

Table of Contents

- Key takeaways

- What is roofing repair credit and its current federal status

- Financing options for roofing repair in Washington state

- Repair or replacement: knowing what financing you actually need

- Practical steps to access roofing repair credits and financing in Washington

- Common misconceptions about roofing repair credit

- My perspective on roofing repair financing after 10 years in this business

- How Atraxroofandgutter can help you finance your roof repair

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Federal credit expired for 2026 | The Section 25C energy credit ended Dec 31, 2025, but 2025 installations can still be claimed on your 2025 tax return. |

| Solar roofing credit is still active | Solar shingles and tiles qualify for a 30% federal credit through 2032, including labor costs. |

| Washington disaster loans available | SBA disaster loans at rates as low as 2.875% are available to homeowners in counties affected by December 2025 flooding. |

| Repair vs. replacement has financial logic | If repair costs reach 30 to 50% of full replacement cost, replacement is usually the smarter financial move. |

| Contractor financing carries hidden risk | Deferred-interest contractor loans can backfire if the balance isn’t paid before the promotional period ends. |

What is roofing repair credit and its current federal status

A roofing repair credit is a tax credit that reduces the amount of federal income tax you owe based on qualifying roofing improvements made to your primary residence. It’s not a discount at the point of sale or a direct payment. It’s a dollar-for-dollar reduction on your tax bill, applied when you file.

The primary federal credit homeowners have relied on is the Section 25C Energy Efficient Home Improvement Credit. This credit covered qualifying cool roofing materials, specifically ENERGY STAR-certified products or roofs meeting the Department of Energy’s cool roof standards. Here’s what you need to know about the current status:

- The Section 25C credit expired on December 31, 2025. No new installations in 2026 qualify under this program.

- If you installed qualifying roofing materials in 2025, you can still claim 30% credit up to $2,500 on your 2025 tax return using IRS Form 5695.

- Labor costs are completely excluded. The 25C credit covers materials only, so your installation labor won’t count toward the credit amount.

- Solar roofing is a different category. If your roof includes solar shingles or tiles that generate electricity, the Section 25D credit remains active through 2032, covers 30% of total costs including labor, and carries no annual cap.

- To claim the 25C credit, you must retain your manufacturer’s certification statement and proof of installation as documentation for the IRS.

The most common misconception right now is that federal roofing credits automatically apply to any repair or replacement project. They don’t. Standard asphalt shingle replacements have never qualified unless the product meets specific energy efficiency criteria.

Pro Tip: If you installed a qualifying cool roof in 2025 but haven’t filed yet, do not miss IRS Form 5695. A $2,500 tax credit is real money, and it applies to your 2025 return even though the program is now expired.

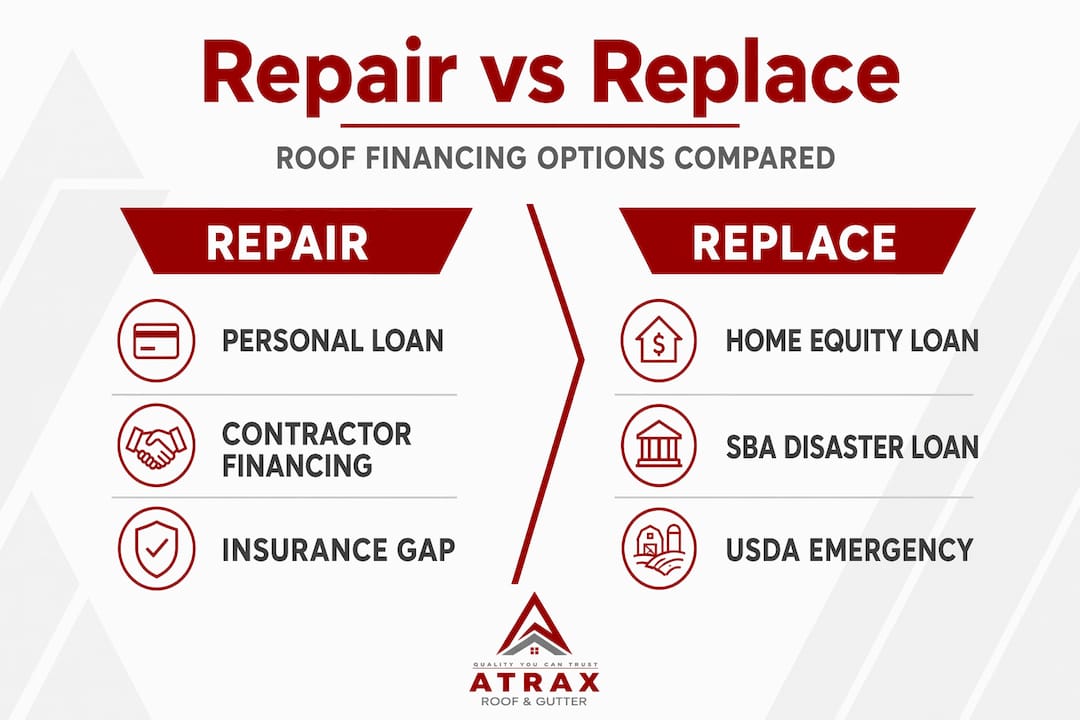

Financing options for roofing repair in Washington state

Understanding roofing repair financing starts with knowing which tools actually fit your situation. Not every homeowner has equity. Not every roof qualifies for disaster assistance. Here’s a clear breakdown of what’s available.

Personal loans

Personal loans are unsecured, meaning you don’t put your home at risk. Funding typically arrives within one to three business days, making them practical when you have a leak and need a contractor this week. The trade-off is higher interest rates compared to equity-based options. If your credit score is strong, you can still find competitive rates. If it’s below 650, expect rates that make a $10,000 loan significantly more expensive over time.

Home equity loans and HELOCs

These products use the equity in your home as collateral, which gives lenders confidence to offer lower rates. The downside is the closing timeline. Home equity products typically take two to four weeks from application to funding. That works fine for a planned replacement but is a poor fit for an emergency.

Contractor-arranged financing

Many roofing contractors offer same-day financing approvals through third-party lenders. It’s convenient. But read the fine print carefully. Contractor financing often includes deferred-interest periods where the promotional 0% APR applies only if you pay the full balance before the deadline. If you carry even a small remaining balance past that date, high interest applies retroactively to the original purchase amount.

Insurance claims and financing gaps

Homeowner’s insurance may cover storm or hail damage, but insurance rarely covers the full cost of a modern roof replacement. You’ll typically need to finance the gap between your insurance payout and the actual project cost. Build that assumption into your budget from the start.

SBA and USDA disaster loans for Washington homeowners

This is where Washington residents have a significant advantage right now. Following the December 2025 atmospheric river flooding, homeowners in affected counties can access SBA disaster loans as low as 2.875% with repayment terms up to 30 years, and loan amounts up to $500,000 for primary residence repairs. For rural Washington homeowners, USDA Section 504 loans start as low as 1% interest, often making them the most affordable roof repair payment option available anywhere.

| Financing type | Typical rate | Approval speed | Collateral required |

|---|---|---|---|

| Personal loan | 8–25% APR | 1–3 days | No |

| Home equity loan | 6–10% APR | 2–4 weeks | Yes (home equity) |

| Contractor financing | 0% promo / high APR after | Same day | No |

| SBA disaster loan | From 2.875% | 2–3 weeks | No (primary residence) |

| USDA Section 504 | From 1% | 3–6 weeks | No |

Pro Tip: If your county was declared a federal disaster area after December 2025 flooding, apply for SBA assistance before pursuing any private loan. The rate difference alone can save thousands over a 10-year repayment period.

Repair or replacement: knowing what financing you actually need

Getting this decision right determines whether you’re financing $1,500 or $15,000. And the math has a clear rule.

- Calculate the repair-to-replacement ratio. Get quotes for both repair and full replacement. If repair costs reach 30 to 50% of what replacement would cost, replacement becomes the financially smarter choice. You get a full system warranty, better energy performance, and no repeated repair bills.

- Check your roof’s age. Asphalt shingle roofs in the Pacific Northwest typically last 20 to 30 years depending on maintenance and exposure. A 22-year-old roof with recurring leaks is rarely worth patching.

- Look at the damage pattern. A single area of missing shingles after a wind event is repair territory. Multiple sections, interior water staining, or granule loss across the entire surface signal system-wide failure.

- Factor in energy costs. An aging roof with poor insulation costs you money every month. A quality roof replacement in Washington is an investment that improves insulation and can lower utility bills.

- Consider the financing implication. A $2,500 repair is manageable with a personal loan or even a credit card if you pay it off quickly. A $14,000 replacement makes sense on a home equity loan or an SBA disaster loan where you lock in a low rate.

Delaying the decision also has a real cost on home value. Deteriorating roofs affect curb appeal, sale readiness, and the structural integrity of everything beneath them.

Practical steps to access roofing repair credits and financing in Washington

Here’s how to move from understanding your options to actually using them.

- Claim the 2025 tax credit if it applies to you. File IRS Form 5695 with your 2025 federal tax return. You’ll need the manufacturer’s certification for your qualifying roofing materials and documentation of the installation date. Work with a tax professional if you’re unsure whether your specific product qualifies.

- Check your county’s FEMA disaster designation. Visit FEMA’s website to confirm whether your county qualifies for individual assistance following the December 2025 storms. If it does, apply for SBA disaster assistance before any private loan.

- Prepare your home equity application. If you have at least 15 to 20% equity in your home, gather your most recent mortgage statement, property tax documents, and two years of tax returns. Most lenders process HELOC applications in two to four weeks.

- Read every line of contractor financing agreements. Know the promotional period end date, the interest rate that applies after that date, and the minimum monthly payment required. If the agreement doesn’t spell these out clearly, ask before you sign.

- Budget for the insurance gap. Financing the gap between your insurance payout and actual replacement cost is common. Get your insurance adjuster’s estimate first, then use that figure as your financing starting point.

- Consult a licensed roofing contractor for an inspection before applying for financing. Knowing the exact scope of work prevents over-borrowing or under-estimating.

Pro Tip: When comparing roof repair loan offers, always calculate the total cost of the loan over its full term, not just the monthly payment. A low monthly payment on a long loan often costs far more in total interest than a higher payment on a shorter term.

Common misconceptions about roofing repair credit

A few persistent misunderstandings cost homeowners real money every year.

- “The federal tax credit still applies in 2026.” It does not. Section 25C expired December 31, 2025. Only 2025 installations claimed on your 2025 return qualify.

- “The credit covers my labor costs.” It never did. The 25C credit excludes labor entirely. Only qualifying material costs count.

- “My insurance will cover everything.” Most policies cover sudden damage, not wear and gradual deterioration. Even for covered events, your deductible and coverage limits usually mean a gap you’ll need to finance.

- “A low credit score means no financing options.” SBA disaster loans and USDA programs consider the disaster context and your ability to repay, not just your credit score. These can be accessible even when traditional lenders say no.

- “I can wait until I have cash.” Delaying roof repairs allows water intrusion to spread to framing, insulation, and drywall. What starts as a $3,000 repair can become a $20,000 structural restoration in 12 to 18 months.

My perspective on roofing repair financing after 10 years in this business

I’ve seen the full range of situations. Homeowners who financed early and protected their homes. Homeowners who waited for the perfect moment and ended up with rotted decking, mold, and a bill three times what the original repair would have cost.

In my experience, the biggest mistake isn’t choosing the wrong financing product. It’s treating financing as a last resort instead of a planning tool. Your roof is one of the most expensive systems in your home. Keeping a financing option ready, whether it’s a HELOC with an available balance or a clear understanding of SBA eligibility, is part of responsible homeownership.

I’m also direct with homeowners about contractor financing. I’ve reviewed those agreements. Some are straightforward and fair. Others are structured so that one missed payment or a balance at the end of the promo period triggers retroactive interest that erases any savings. Read those terms with the same care you’d give a mortgage.

For Washington homeowners right now, I genuinely believe the SBA disaster loan program is underutilized. If your county qualifies and you have roof damage from the December 2025 flooding, a 2.875% rate on a 30-year term is a financial advantage you shouldn’t leave on the table. Call your county’s disaster assistance office before you call a private lender.

My bottom line: don’t wait, don’t guess, and don’t sign anything you don’t fully understand. Partner with a roofing professional who will be honest with you about what your roof actually needs, and then match that to the right financing option.

— Danyllo

How Atraxroofandgutter can help you finance your roof repair

When you’re ready to move forward, Atraxroofandgutter makes the process straightforward. We work with Washington homeowners across Kirkland, Bothell, Redmond, Bellevue, Seattle, and surrounding communities to find roofing repair financing that fits your actual situation, not a one-size-fits-all pitch.

Our team will assess your roof honestly, explain exactly what work is needed, and walk you through every financing option available to you, including contractor financing, personal loan referrals, and guidance on applying for SBA disaster assistance if your county qualifies. We use only premium GAF and CertainTeed materials, and every project is backed by our 20-year workmanship warranty. No surprise costs. No pressure. You can also browse our completed projects portfolio to see the quality we deliver before you commit.

Contact Atraxroofandgutter today for a free, no-obligation inspection and financing consultation. Protecting your family starts with knowing your roof is sound and knowing you can afford to keep it that way.

FAQ

What is roofing repair credit exactly?

A roofing repair credit is a federal or state tax credit that reduces your income tax owed based on qualifying roofing improvements. The main federal program, Section 25C, expired December 31, 2025, but solar roofing credits under Section 25D remain active through 2032.

Can I still claim a roofing tax credit in 2026?

You can only claim the Section 25C credit for roofing materials installed in 2025, filed on your 2025 tax return using IRS Form 5695. No new standard roofing installations in 2026 qualify for a federal energy credit.

Does the roofing credit cover labor costs?

No. The Section 25C credit covers qualifying material costs only. Labor and installation fees are excluded entirely from the credit calculation.

What roof repair payment options are available in Washington state?

Washington homeowners can access personal loans, home equity loans or HELOCs, contractor financing, and, for counties affected by the December 2025 flooding, SBA disaster loans starting at 2.875% APR with terms up to 30 years.

When does it make more financial sense to replace than repair a roof?

When repair estimates reach 30 to 50% of the total replacement cost, a full replacement is typically the better financial decision. It avoids repeated repair costs and gives you a full system warranty and longer lifespan.